Tax Hotline: Treaty Shopping and GAAR: Learnings from Canada for India

Posted by By nishithadmin at 17 October, at 17 : 29 PM Print

TREATY SHOPPING AND GAAR: LEARNINGS FROM CANADA FOR INDIA

- Canadian Court rules Luxembourg resident investment holding company entitled to exemption from Canadian capital gains tax under treaty;

- Claiming exemption did not amount to misuse or abuse of the treaty, GAAR inapplicable

- Treaty shopping permissible absent rule to the contrary

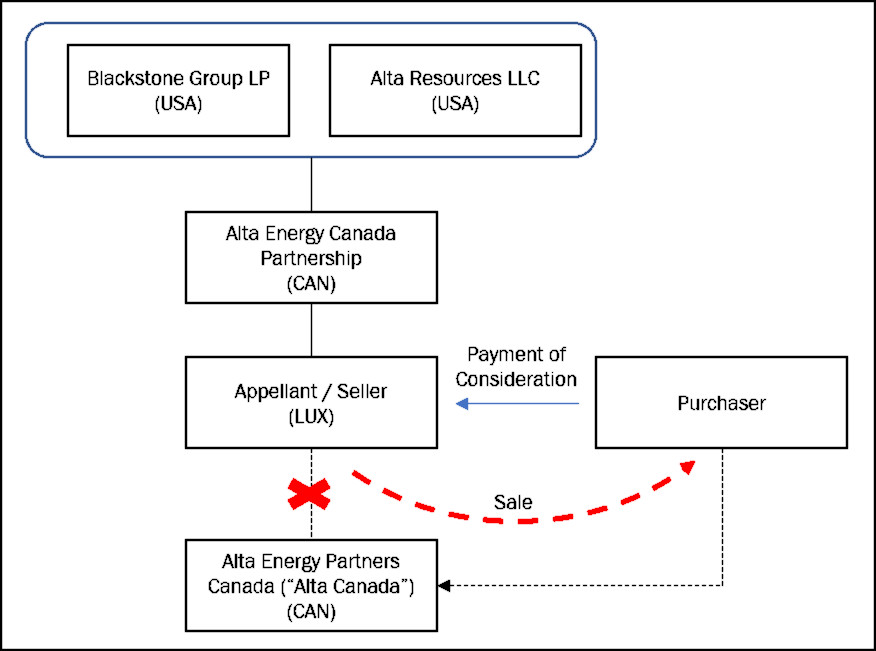

Recently, on August 22, 2018, a Canadian Tax Court (“Court”) ruled that a capital gain arising on the sale (“Sale”) of shares (“Shares”) of Alta Energy Partners Ltd (“Alta Canada”) was not taxable in the hands of Alta Energy Luxembourg SARL (“Appellant” or “Seller”), under Article 13(5) of the Canada-Luxembourg Tax Treaty (“Treaty”). Holding that the gain would not be covered under Article 13(4) of the Treaty, the Court concluded that granting the exemption under Article 13(5) to the Seller constituted neither an abuse nor a misuse of the provisions of the Canadian Income Tax Act (“CITA”) or the Treaty, and would therefore not be hit by the provisions of Canada’s General Anti-Avoidance Rule (“GAAR”).

The Sale is diagrammatically depicted below:

BACKGROUND

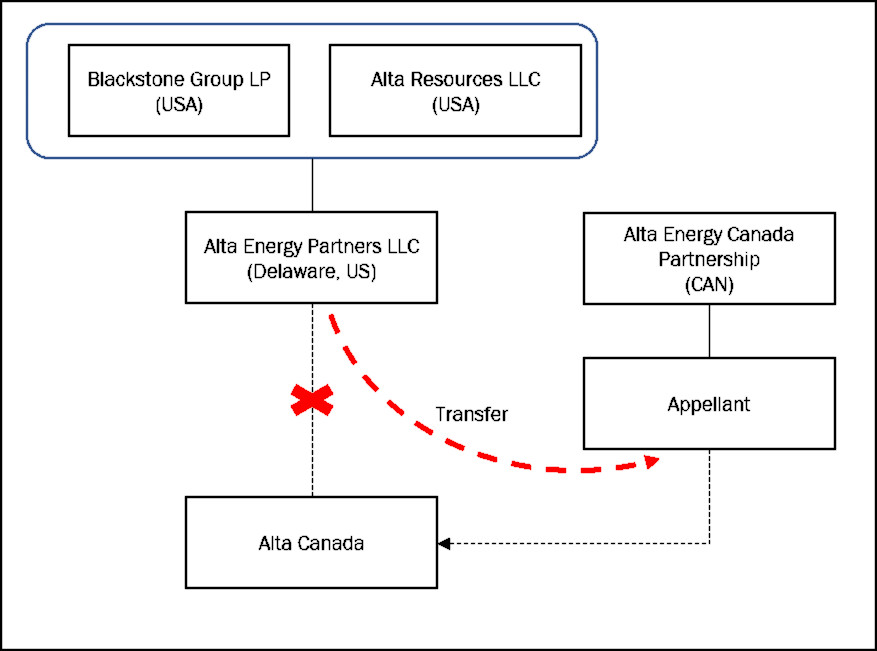

In 2011, the Blackstone Group LP, an American multinational private equity, alternative asset management and financial services firm, and Alta Resources LLC, a leading American company engaged in the exploration for and development of shale oil and gas assets in the USA and Canada, formed Alta Energy Partners LLC (“Alta LLC”), as a Delaware LLC to acquire and develop unconventional oil and natural gas properties in North America (the Blackstone group LP and Alta Energy Partners LLC are hereinafter collectively referred to as the “Co-Investors”).

The Co-Investors then incorporated Alta Canada as a wholly owned subsidiary of Alta LLC to develop the Duvernay shale oil formation (“Duvernay Formation”) situated in Northern Alberta. Alta Canada was granted the right to explore, drill and extract hydrocarbons from an area of the Duvernay Formation (Alta Canada’s “Working Interest”) designated under licenses (“Licenses”) granted by the government of Alberta.

However, this initial structure proved to be sub-optimal from an overall tax perspective, and needed to be revised to mitigate the impact of US Subpart F anti-deferral provisions.1 Accordingly, in 2012, the Appellant was incorporated in Luxembourg, as a wholly owned subsidiary of Alta Energy Canada Partnership, a partnership established under the laws of Canada. Shortly thereafter, Alta LLC transferred shares of Alta Canada to the Appellant.2 Thus the structure prior to the Sale came into being.

The restructuring (“Restructuring”) leading to the transition from the initial structure to the revised structure is diagrammatically depicted below:

At the time of the Sale, in keeping with industry practice, Alta Canada had commenced drilling only in certain sections of the Working Interest.3

RELEVANT PROVISIONS

Article 13(4) of the Treaty. Under Article 13(4), Canada has the right to tax capital gains arising from the disposition of shares that derive their value principally from immovable property (“Immovable Property”) situated in Canada. The application of Article 13(4) is subject to an important exception – property that would otherwise qualify as Immovable Property is deemed not to be such property in the circumstances where the business of the corporation is carried on in the property (the “Excluded Property” exception).

Article 13(5) of the Treaty. Article 13(5) is a distributive rule of last application. It applies only in cases where capital gains are not otherwise taxable under paragraphs (1) to (4) of Article 13 of the Treaty.

Section 245(2) of the CITA. Section 245(2) provides that “Where a transaction is an avoidance transaction4, the tax consequences to a person shall be determined as is reasonable in the circumstances in order to deny a tax benefit that, but for this section, would result, directly or indirectly, from that transaction or from a series of transactions that includes that transaction.”

Section 245(4) of the CITA. Section 245(4) provides that section 245(2) applies to a transaction only where it may reasonably be considered that the transaction would result directly or indirectly in a misuse of the provisions of inter alia the CITA or a tax treaty.

ISSUES

- Is the capital gain realized by the Appellant as a result of the sale of the shares taxable in Canada in view of Article 13(4) of the Treaty?

- Does the GAAR apply to override the application of the Treaty?

ARGUMENTS OF THE CANADIAN TAX DEPARTMENT

- The Tax Department argued that substantially all of Alta Canada’s Working Interest constituted Immovable Property for the purposes of Article 13(4) of the Treaty because Alta Canada drilled in and extracted hydrocarbons from only a small area of the Duvernay Formation that it controlled. The Tax Department contended that the use of the word “in” in Article 13(4) of the Treaty, instead of “by which”, “with which”, or “through which”, imply that it is not enough for the property to be used in the business, but that the business must be carried on within the physical limits of the property.

- The Tax Department also contended that even if the Working Interest constituted Excluded Property, the GAAR would apply to deny the Appellant the exemption under Article 13(5). In addition to constituting an abuse of the provisions of the CITA, the Tax Department argued that the Restructuring resulted in an abuse of the Treaty, since the Treaty was intended to prevent double taxation and fiscal evasion, and in this case, the Appellant was paying tax neither in Luxembourg nor Canada. The Tax Department further sought to establish that there was a misuse / abuse of the Treaty by arguing that the Appellant, although a resident of Luxembourg for the purposes of Article 4 of the Treaty, was created and became the owner of the shares of Alta Canada for no purpose other than to avoid Canadian income tax on the gain that it realized on the Sale, and was therefore a conduit company, created solely for the purpose of passing on the tax benefit (i.e., exemption from Canadian capital tax) to its shareholders who would otherwise not be entitled to claim the benefits of the Treaty in their own right. The Tax Department argued that this amounted to treaty shopping, which was tantamount to a misuse or abuse of the Treaty.

ARGUMENTS OF THE APPELLANT

- The Appellant conceded that while the shares of Alta Canada derived their value principally from the Working Interest, the Working Interest constituted Excluded Property for the purposes of Article 13(4).

- While the Appellant conceded that it derived a tax benefit5 from the Restructuring from the sale of Alta Canada from Alta LLC to the Appellant, and that the Restructuring was not arranged primarily for a bona fide purpose other than to obtain a tax benefit, and thus qualified as an avoidance transaction, the Restructuring did not amount to a misuse or abuse of the provisions of the CITA or the Treaty, so as to trigger the application of the GAAR.

RULING

- Is the capital gain realized by the Appellant as a result of the sale of the shares taxable in Canada in view of Article 13(4) of the Treaty?

Noting that under the CITA, Canadian income tax is payable on gains realized from the disposition of “taxable Canadian property” that is not “treaty protected property” (as defined in the CITA), the Court held that while the shares of Alta Canada constituted “taxable Canadian property” because the shares of Alta Canada derived more than 50% of their value from the Working Interest, which is a Canadian resource property,6they also constituted “treaty protected property”7.

Rejecting the Tax Department’s interpretation of Article 13(4), and recognizing that that such an interpretation would not be workable in the context of the natural resource sector, given the nature of the sector, the Court held that in order for a reserve to constitute Excluded Property, it would suffice that its owner was actively engaged in its exploration, and that it was being actively exploited or being kept for future exploitation.

- Does GAAR apply to override the application of the Treaty?

In keeping with precedent, the Court employed a two-step process to determine whether there was an abuse or misuse, namely:

(a) identifying the object, spirit and purpose of the relevant rule;

(b) determining whether the avoidance transaction falls within, or frustrates, that rationale.

In this regard, the Court held that the Restructuring would not amount to an abuse or misuse of the CITA, considering that the provisions regarding taxation of gains arising on the transfer of Canadian taxable property were not intended to operate in the context of a non-resident realizing gains on the transfer of “treaty protected property”, which the Court had already held the Working Interest to be.

On the aspect of whether the Restructuring amounted to an abuse or misuse of the Treaty, the Court chose to identify and be guided by the specific rationale underlying Article 1, 4 and 13, instead of what it termed “the vague policy supporting a general approach to the interpretation of the Treaty as a whole” set out in the preamble8.

Noting that in order for Article 13(4) and (5) of the Treaty to apply, the Appellant needed to be a resident of Luxembourg and, finding that the Appellant met the requirements set out in Article 4 to qualify as a resident of Luxembourg, the Court ruled that in the absence of any further limitation denying a claimant access to treaty benefits (as exists in many of Canada’s other tax treaties), it could not be said that there was an abuse / misuse of the Treaty and, the exemption could not be denied to the Appellant.

The Court further noted that the OECD Model Tax Convention does not contain an exception of the nature set out in Article 13(4) of the Treaty, and that were the parties had chosen to intentionally depart from the text of the Model Tax Convention, it was not the role of the Court to disturb the bargain of the parties in this regard.

The Court further noted that contracting parties are presumed to understand the other country’s tax system when they negotiate a tax treaty and that if Canada wished to curtail the benefits of the Treaty to potential situations of double taxation, Canada could have insisted that the exemption provided for under Article 13(5) be made available only in the circumstance where the capital gain was otherwise taxable in Luxembourg.

The Court also rejected the argument that the Appellant was a conduit company. The Court noted that “a corporation is often referred to as a “conduit” when it holds property for a principal” and that in such case, “the principal is the “beneficial owner” of the property’s legal title is in the name of the corporation which holds title as an agent or nominee for the principal.” The Court held that the fact that the Tax Department had chosen to assess the gains to tax in the hands of the Appellant implied that it had accepted the Appellant as the beneficial owner.

Recognizing that holding corporations are often established for a single purpose which includes the holding of shares of a single corporation, the Court held that there was nothing unusual about the fact that the Appellant held the shares for a relatively short period of time, sold them when the Co-Investors wished to do so, and distributed the proceeds to its shareholders.

The Court found that there is nothing in the Treaty that suggests that a single purpose holding corporation, resident in Luxembourg, cannot avail itself of the benefits of the Treaty, or that a holding corporation, resident in Luxembourg, should be denied the benefit of the Treaty because its shareholders are not themselves residents of Luxembourg.

Lastly, the Court ruled that in the absence of a specific anti treaty shopping rule in the Treaty9 the denial of the exemption would amount to denial of benefit criteria other than residence, which is not permissible.

ANALYSIS

A well-known and well established general principle regarding the relationship between tax treaties and the CITA is that Canadian tax treaties generally prevail over the provisions of the CITA to the extent of any inconsistency, subject to the provisions of the Income Tax Conventions Interpretation Act (“ITCIA”).10 Section 4.1 of the ITCIA is a non-obstante clause that allows for the application of the GAAR notwithstanding the provisions of a tax treaty or the legislation giving that tax treaty the force of law in Canada.

This mechanism is very similar to the manner in which India’s General Anti Avoidance Rule (“Indian GAAR”) has been engineered to apply to India’s tax treaties – essentially section 95 of the Income Tax Act, 1961 (“ITA”) is a non-obstante clause that allows the Indian GAAR to apply notwithstanding the provisions of section 90 of the ITA.11

However, unlike the Canadian GAAR, the applicability of which rests on (a) the existence of a transaction resulting in a tax benefit (except where the transaction can also be reasonably considered to have been undertaken for primarily bona fide purposes other than to obtain a tax benefit) and (b) such transaction involving an abuse or misuse of the provisions of the CITA or a tax treaty, the Indian GAAR requires (a) that a transaction be entered into with the ‘main’ purpose of obtaining a tax benefit and (b) such transaction also (i) create rights, or obligations, which are not ordinarily created between persons dealing at arm’s length, (ii) result, directly or indirectly, in the misuse, or abuse of the provisions of the ITA, (iii) lack commercial substance or (iv) be entered into or carried out, by means, or in a manner, which is not ordinarily employed bona fide purposes.

The instant case deals with a structure created admittedly solely to obtain a tax benefit. However, as with the Indian GAAR, under the Canadian GAAR, it is not sufficient that a transaction be entered into solely, or even primarily to obtain a tax benefit, but also that the transaction result in a misuse or abuse of the treaty or relevant domestic tax law (the Indian GAAR is possibly wider in this sense, as in addition to a misuse or abuse, the Indian GAAR provides for other circumstances in which the GAAR may also be triggered). Accordingly, the Court analyzed whether the Restructuring amounted to an abuse or misuse of the provisions of the CITA and the Treaty.

Given the similarities between the GAAR and the Indian GAAR, the Court’s analysis provides an insight on the manner in which the Indian GAAR should be applied.

- Residence. The Court upheld the widely accepted practice12 that a person fulfilling the requirements of Article 4 of a tax treaty i.e., being a person liable to tax under the laws of one of the contracting countries by reason of its domicile, residence, place of management or any other criterion of a similar nature, is generally entitled to claim the benefits of the treaty accorded to residents of that country. The Court held that in the absence of express language in the Treaty requiring additional criteria to be fulfilled, such limitations cannot be implied into the Treaty to deny benefits to the Appellant.

Since the landmark ruling of the Indian Supreme Court in Azadi Bachao Andolan13, Indian courts have also generally allowed treaty benefits where the residence of the claimant has been satisfactorily established (often with the aid of a tax residency certificate).

- Beneficial Ownership & Conduit Status. The Court displayed a nuanced understanding of commonly used fund investment structures, and recognized that holding corporations are often established for a single purpose which could include the holding of shares of a single corporation. The fact that such corporations dispose of their investment holdings when advantageous distribute the sale proceeds to their shareholders, would not automatically amount such corporations conceding beneficial ownership of the investments to their shareholders, and becoming mere conduits. Such actions merely take into account the purpose for which such corporations are created and the intent of their shareholders.”

Of course, it is likely that the existence of a flawless paper trail played a role in the Court’s conclusion decision and it is worth mentioning here that there have been Indian cases14 where Indian courts have denied treaty benefits to special purpose vehicles incorporated solely to hold investments in Indian companies on grounds that they lacked substance or were not the beneficial owners of their Indian investments. While beneficial ownership is not an express requirement of the “Capital Gains” Article of most tax treaties, the Supreme Court of India and High Courts have, over the years, distilled a judicial anti-avoidance doctrine, which allows tax benefits to be disallowed in the case “sham transactions” or “colourable devices” i.e., transactions involving dubious methods, subterfuge or an act of which the judicial process may not accord approval. In these cases, the lack of sufficient evidence establishing beneficial ownership played a key role in the courts decision.

- Treaty Shopping. Much in the same vein as the Supreme Court ruling in Azadi, the Court held that, where the conditions prescribed under the a treaty for availing benefits were fulfilled, in the absence of an anti-treaty shopping or rule of similar nature, treaty shopping was not per se illegal.

NEXT STEPS?

The Canadian approach in this case should give a good indicator for Indian tax authorities and courts on how to approach the Indian GAAR. While the Indian GAAR provides for treaty override, the approach of the Court indicates that a cautious view has to be taken in such cases with the test to be applied not only being whether a taxpayer has obtained a tax benefit, but also whether such benefit amounted to a misuse or abuse of a provision, or was not in accordance with the true object, spirit and purpose of that provision.

However, with the impending onset of the Multilateral Instrument (“MLI”), it becomes interesting to analyze whether the Court would have concluded differently had the MLI already been in effect. Article 6 of the MLI proposes to introduce, as a minimum standard, the following preamble to all covered tax treaties (“CTAs”):

“Intending to eliminate double taxation with respect to the taxes covered by this agreement without creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance (including through treaty shopping arrangements aimed at obtaining reliefs under the agreement for the indirect benefit of residents in third jurisdictions).” [Emphasis added]

India has been silent on its position on Article 6. Therefore, in the absence of India notifying any treaty provisions/preamble language, the MLI Preamble will not replace the existing preamble language in India’s CTAs but will only be added to the existing preamble text, irrespective of whether or not its treaty partners notify their treaty with India for this purpose. The revised preamble is likely to have considerable bearing on the manner in which Indian court’s view structures of the nature involved in the present case, and is likely to strengthen arguments that such structures amount to an abuse of the provisions of treaties, triggering the Indian GAAR.

Article 7 of the MLI also requires countries to, as a minimum standard, implement at least one of the following anti-abuse measures in their CTAs: – (i) a principal purpose test (“PPT”) only, which is a general anti-abuse rule based on the principal purpose of transactions or arrangements (ii) a PPT supplemented with either a simplified or a detailed limitation on benefits (“LOB”) provision, or (iii) a detailed LOB provision, supplemented by a mutually negotiated mechanism to deal with conduit arrangements not already dealt with in tax treaties.

The PPT has been introduced as a default test which provides that no benefit under the CTA shall be granted if it is reasonable to conclude that obtaining that benefit was one of the principal purposes of any arrangement or transaction that resulted directly or indirectly in that benefit. However, most importantly, there is a carve out for granting such treaty benefits if availing such benefits was is in accordance with the object and purpose of the relevant provisions of the CTA. It will fall to the courts to determine whether the granting of benefits is in accordance of the objects and purpose of a treaty.

The changes brought about by the MLI will also no doubt result in changes to the manner in which the Indian tax authorities and courts approach issues of treaty shopping and beneficial ownership, as well as the manner in which the Indian GAAR is applied.15

In the meantime, funds and investors will need to ensure that other criteria, such as the availability of directors with knowledge of regional business practices and regulations, the existence of a skilled multilingual workforce, a jurisdiction’s membership of a regional grouping and use of the regional grouping’s common currency etc. play a central role in selecting a jurisdiction for incorporating a special purposes investment holding vehicle or intermediary holding entity.

1Witness testimony presented during the court proceedings establish that the initial structure was set up on the assumption that the Co-Investors would acquire and develop resource properties situated in the USA, not Canada.

2The transfer of Shares from Alta LLC to the Appellant gave rise to a taxable capital gain. However, the CRA accepted that the fair market and the adjusted cost base of the Shares were equal at that time. The Co-Investors would, undoubtedly, have incurred significant legal costs in connection with the transfer.

3 This was due to a number of reasons including (a) the nature of conventional oil extraction is such that since oil is often present in a large pool, a vertical well on a particular section of a formation often allows the operator to extract oil from many of the sections where no drilling takes place; (b) initial drilling is done on a trial and error basis, and only once the best drilling methods are identified and documented, the same methods are used to drill wells elsewhere in the formation.

4 Section 245(3) of the CITA provides that “An avoidance transaction means any transaction (a) that, but for this section, would result, directly or indirectly, in a tax benefit, unless the transaction may reasonably be considered to have been undertaken or arranged primarily for bona fide purposes other than to obtain the tax benefit; or (b) that is part of a series of transactions, which series, but for this section, would result, directly or indirectly, in a tax benefit, unless the transaction may reasonably be considered to have been undertaken or arranged primarily for bona fide purposes other than to obtain the tax benefit.”

A “tax benefit” is defined as “a reduction, avoidance or deferral of tax or other amount payable under this Act or an increase in a refund of tax or other amount under this Act, and includes a reduction, avoidance or deferral of tax or other amount that would be payable under this Act but for a tax treaty or an increase in a refund of tax or other amount under this Act as a result of a tax treaty.”

5 The Exempt Property exception does not exist under the Canada-USA Tax Treaty, and it is likely that tax on the gains realised on sale of shares of Alta Canada would have been taxable in Canada if the Co-Investors or Alta LLC had invested in Alta Canada directly. As a result of the Restructuring, under the Treaty, the gains were taxable neither in Canada nor Luxembourg.

6 Shares of a company generally constitute “taxable Canadian property” if, at the time of their disposition, or during the 60 months that ended prior to that time, more than 50% of the fair market value of the share was derived, inter alia, directly or indirectly from or any combination of: (i) “real or immovable property situated in Canada”, (ii) “Canadian resource properties”, (iii) “timber resource properties”, and (iv) options in respect of interests in any of the aforementioned properties.

7 Under the CITA “treaty protected property” means property, any income or gain from the disposition of which, by the taxpayer, would, because of a tax treaty with another country, be exempt from tax under Part I of the CITA.

8 “to conclude a Convention for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and on capital.”

9 See the Canada-USA Tax Treaty.

10 See: “The Relationship Between Tax Treaties and the Income Tax Act: Cherry Picking”, Arnold, Brian J., Canadian Tax Journal, (1995), Vol.43, No.4

11 Section 90 of the ITA provides for the provisions of a tax treaty to apply to a taxpayer where they are more beneficial than the provisions of the ITA.

12 Notable exceptions to this general principle can be found in the context of dividends (Article 10), interest (Article 11) and royalties (Article 12), where in addition to residence, treaties require a recipient of such payments to also establish itself as the beneficial owner of such amounts in order to claim treaty benefits.

13 [2002] 125 TAXMAN 826 (SC)

14 See: AB Mauritius, In re 402 ITR 311; Also see: Aditya Birla Nuvo v. DDIT, Bombay High Court, W.P. No.730 OF 2009, where the Bombay High Court allowed the Indian tax authorities to investigate the bona fides of a Mauritius resident claiming benefit under the India-Mauritius Tax Treaty, but did not deal with merits of the claimants eligibility to avail relief.

15 It is also worth noting that India has already introduced generic LOBs in a number of its tax treaties.[1] By and large, these LOBs provide for the denial of treaty benefits where the affairs of the claimant were arranged with the main purpose of obtaining such benefit. However, the LOB proposed to be introduced by the MLI is more detailed and comprehensive and is likely to increase the potential for investing holding companies to be denied treaty benefits, unless they can demonstrate appropriate substance.

Chambers and Partners: Ranked in Tier 1 for Tax

World Tax (International Tax Review’s Directory): Recommended Tax Firm in India

Legal 500 2018 : Ranked in Tier 1 for Dispute Resolution, Labour & Employment, Investment Funds, TMT and Tax

Fastest Growing M&A Law Firm in India in 2015: MergerMarket

The Most Innovative Law Firm in Asia-Pacific

![]()

DISCLAIMER

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

")

")

")