Funds Hotline: SEBI releases AIF (Second Amendment) Regulations, 2021

Posted by By nishithadmin at 14 May, at 13 : 39 PM Print

Warning: count(): Parameter must be an array or an object that implements Countable in /web/qlc/nishith.tv/htdocs/wp-content/themes/Video/single_blog.php on line 46

Warning: count(): Parameter must be an array or an object that implements Countable in /web/qlc/nishith.tv/htdocs/wp-content/themes/Video/single_blog.php on line 52

SEBI RELEASES AIF (SECOND AMENDMENT) REGULATIONS, 2021

BACKGROUND

The Securities and Exchange Board of India (“SEBI”) recently released the SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2021 (“Amendment Regulations”). The Amendment Regulations are in furtherance of SEBI’s board meeting, dated March 25, 2021 (“Board Meeting”) where certain amendments were proposed to SEBI (Alternative Investment Funds) Regulations, 2012 (“AIF Regulations”).

A summary of the changes introduced by the Amendment Regulations is provided below, along with our analysis. We had also discussed most of these amendments (when they were at the proposal stage in the Board Meeting) in our monthly digest for April 2021 which is available here.

ANGEL FUNDS, START-UPS AND VCUS

- “Start-up” has been defined to mean an entity which fulfils the criteria for start-up as specified by the Department for Promotion of Industry and Internal Trade (“DPIIT”), vide notification No. G.S.R. 127(E), dated February 19, 20191 or such other policy of the Central Government issued in this regard from time to time (“Start-up”). This should lead to elimination of uncertainty around the scope of the term “start-up” and harmonise its usage with that by the other regulators.

- Angel funds, as a sub-category of a Venture Capital Fund under Category I AIF, are now eligible to invest in Start-ups, rather than VCUs as earlier described under Regulation 19F(1) of the AIF Regulations. This amendment broadens the investment horizon of angel funds as now these funds can invest in an entity which, inter alia, (a) has not crossed 10 years and (b) whose turnover has not exceeded INR 100 crores in any of the financial years, beginning from the date of such entity’s incorporation or registration.

However, corresponding amendments to sub-regulations (2), (3), (5) of Regulation 19F and sub-regulation (3) of Regulation 19G have not been made. Accordingly, in order to provide complete clarity in this respect, the requisite changes to the foregoing provisions should also be made.

- The scope of the definition of Venture Capital Undertaking (“VCU”) has been broadened for Category I AIFs by removal of the list of restricted activities in the definition of a VCU. This should enable Category I AIFs to now allocate monies towards NBFCs which was earlier prohibited.

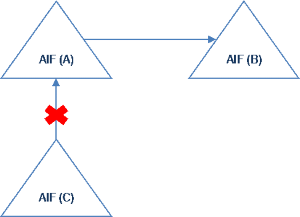

INVESTMENT IN OTHER AIFS

- AIFs have been permitted to invest in an investee company, directly or through other AIFs, subject to diversification limits of (a) 25% (of investible funds) for Category I and II AIFs; and (b) 10% (of investible funds) of Category III AIFs.

- An AIF investing in other AIFs is not further permitted to have an AIF as its investor. AIFs which employ fund-of-funds strategy should henceforth seek a confirmation from their investee AIFs that such investee AIFs will not further be investing in other AIFs.

- For an AIF to invest in units of AIFs managed / sponsored by its AIF manager / sponsor or associates of its AIF manager / sponsor, a prior approval of at least 75% of the investors by value of their investment in such AIF is now required.

- The investment by an AIF in other AIF shall have to be in the following manner: (i) a Category I AIF can invest in units of other Category I AIFs of the same sub-category; (ii) a Category II AIF can invest in Category I or II AIF; and (iii) a Category III AIF can invest in units of Category I, II or III AIFs.

CODE OF CONDUCT

- Similar to respective codes of conduct specified for different market intermediaries, SEBI has now prescribed a code of conduct for AIFs, AIF managers, their key management personnel, AIF trustees, directors of the AIF trustee and the members of the investment committee (“ICOM”), if any, (“Code of Conduct”) under the Fourth Schedule of the Amendment Regulations.

- The Amendment Regulations provide that the AIFs are required to have policies and procedures, approved jointly by the AIF manager and the AIF trustee, in place. The AIF manager shall be responsible to ensure that every decision of the AIF is in compliance with such policies and procedures, the AIF Regulations, terms of the private placement memorandum (“PPM”), other AIF documents and the applicable laws. Unlike other jurisdictions, the PPM has a regulatory relevance for AIFs even though it may not have any binding value contractually.

- Further, in order to provide clarity on the scope of responsibilities casted on the ICOM, the Amendment Regulations stipulate that the ICOM members shall ensure that their decisions are also in compliance with the policies and procedures of the AIF, provided that a waiver can be obtained in this regard by AIFs where each investor has a capital commitment of at least INR 70 crores to each such AIF. ICOM members may not be jointly liable with AIF managers due to the Amendment Regulations; however, SEBI seems to have retained regulatory authority over such members. Depending on the exact scope of the ICOM, it should be determined whether the ICOM is carrying on fiduciary duties.

- The Amendment Regulations have retained the requirement of prior consent of 75% of the investors by value of their investment in an AIF in a situation where an external member, whose name is not disclosed in the PPM or any other AIF document at the time of on-boarding of investor(s), is being appointed on the ICOM.

The above changes reflect the market regulators’ continual approach to strike a balance between accountability of the AIF managers towards the investors and the flexibility such managers would need to effectively run their operations.

1 Department for Promotion of Industry and Internal Trade Notification dated February 19, 2019, available at https://www.startupindia.gov.in/content/dam/invest-india/Templates/public/198117.pdf.

Benchmark Litigation Asia-Pacific:Tier 1 for Government & Regulatory and Tax

2020, 2019, 2018

Legal500 Asia-Pacific:Tier 1 for Tax, Investment Funds, Labour & Employment and TMT

20a20, 2019, 2018, 2017, 2016, 2015, 2014, 2013, 2012

Chambers and Partners Asia-Pacific:Band 1 for Employment, Lifesciences, Tax and TMT

2020, 2019, 2018, 2017, 2016, 2015

IFLR1000:Tier 1 for Private Equity and Project Development: Telecommunications Networks.

2020, 2019, 2018, 2017, 2014

AsiaLaw Asia-Pacific Guide 2020:Ranked ‘Outstanding’ for TMT, Labour & Employment, Private Equity, Regulatory and Tax

FT Innovative Lawyers Asia Pacific 2019 Awards: NDA ranked 2nd in the Most Innovative Law Firm category (Asia-Pacific Headquartered)

RSG-Financial Times: India’s Most Innovative Law Firm

2019, 2017, 2016, 2015, 2014

Who’s Who Legal 2020:

• Nishith Desai- Thought leader (Corporate Tax 2020, India 2020), Global leaders

(Private Funds 2020)

• Vikram Shroff-Global Leaders (Labour & Employment 2020, Pensions & Benefits 2020)

• Milind Antani- Pharma & Healthcare – only Indian Lawyer to be recognized for

‘Life sciences – Regulatory,’ for 5 years consecutively

DISCLAIMER

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

")

")

")

")